I recommend implementing a thorough inventory bookkeeping system that combines proper accounting methods (FIFO, LIFO, or weighted average), regular physical counts, and detailed transaction documentation. You’ll need to establish systematic counting procedures, utilize barcode scanning for accuracy, and maintain meticulous records of all inventory movements. Track key metrics like turnover ratios and carrying costs through an integrated tracking system. The right combination of these practices will transform your inventory management efficiency.

Choose the Right Inventory Accounting Method

Selecting an appropriate inventory accounting method is essential for accurate financial reporting and tax compliance. I’ll help you master the three primary methods: FIFO, LIFO, and weighted average cost.

FIFO (First-In-First-Out) works best in industries with perishable goods or rapid product turnover. I recommend LIFO (Last-In-First-Out) when you’re operating in an inflationary market and want to minimize taxable income. For stable-priced commodities, weighted average provides the most straightforward calculation.

Your choice will impact your balance sheet, tax obligations, and profit margins. I advise reviewing your industry standards and consulting your tax advisor before implementation.

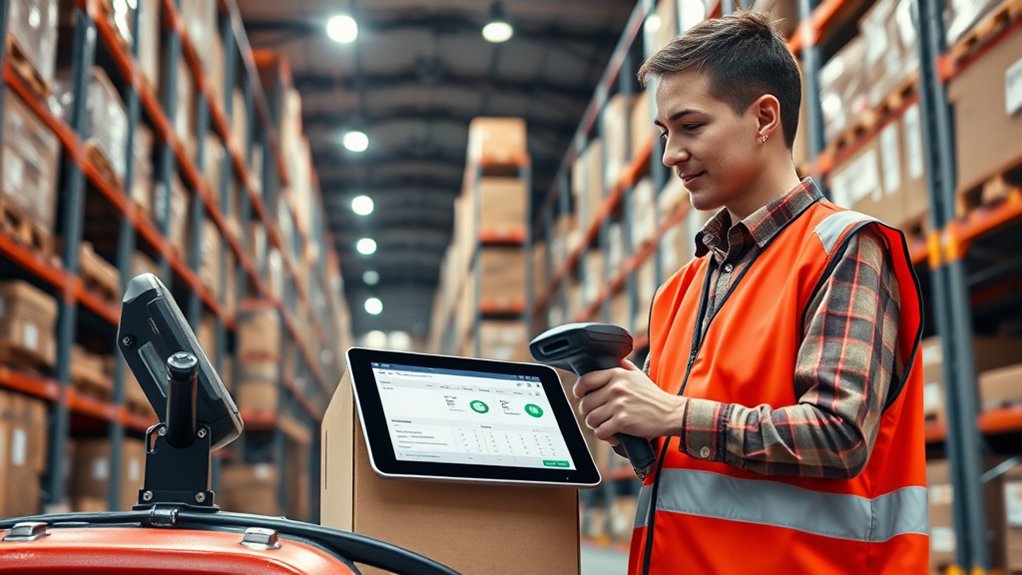

Implement Regular Inventory Counting Procedures

Regular inventory counting forms the backbone of accurate bookkeeping and financial control. I recommend implementing a dual-counting system: frequent cycle counts for high-value items and annual exhaustive counts for your entire inventory.

I’ll emphasize that you must document each count meticulously using standardized forms. Track variances between book and physical counts, investigating discrepancies immediately. I’ve found that barcode scanners and inventory management software dramatically reduce human error.

Schedule counts during off-peak hours and assign clear roles to your counting teams. Don’t forget to maintain strict segregation of duties between counters and record-keepers to guarantee count integrity.

Document All Inventory Movements and Transactions

Thorough documentation of inventory movements serves as a critical control mechanism for maintaining accurate stock records. I recommend implementing a robust transaction logging system that captures every receipt, transfer, and dispatch of items. You’ll need to record essential data points including dates, quantities, locations, personnel, and reference numbers.

I’ve found that utilizing barcode scanning and automated data entry dramatically reduces documentation errors. You must guarantee all stakeholders input real-time updates for purchases, sales, returns, and internal transfers. This creates an unbroken chain of custody and enables you to trace any discrepancies to their source, strengthening your inventory control.

Set Up an Efficient Inventory Tracking System

To optimize inventory management, you’ll need a systematic tracking approach that combines software tools, identification methods, and location mapping.

I recommend implementing a barcode or RFID system integrated with enterprise resource planning (ERP) software. This enables real-time tracking, minimizes human error, and accelerates data collection. Establish clear storage zones with alphanumeric identifiers and maintain a digital mapping system that pinpoints item locations instantly.

Configure automated alerts for reorder points, stock-outs, and slow-moving inventory. Track key metrics like turnover rates, holding costs, and shrinkage. Regular system audits guarantee accuracy and identify opportunities for process improvements in your inventory control framework.

Monitor Key Inventory Metrics and Reports

Building upon your established tracking system, effective inventory management hinges on monitoring specific performance indicators and generating actionable reports.

I recommend tracking these critical metrics: inventory turnover ratio, gross margin ROI, stock-to-sales ratio, and carrying costs. You’ll want to analyze stockout rates, lead times, and demand forecasting accuracy. Generate weekly reports on slow-moving items, dead stock, and reorder points.

I’ve found that monitoring these KPIs enables you to optimize working capital, reduce holding costs, and maintain ideal stock levels. Leverage these metrics to make data-driven decisions about purchasing, pricing, and stock allocation strategies.

Establish Internal Controls for Inventory Management

Strong internal controls form the backbone of reliable inventory management systems. I recommend implementing rigorous protocols that safeguard your assets while maintaining operational efficiency. Your control system must establish clear accountability and minimize risks of theft, damage, or misreporting.

- Segregate duties between receiving, storing, and recording inventory to prevent unauthorized access and manipulation

- Create standardized documentation procedures for all inventory movements, requiring dual signatures on critical transactions

- Implement restricted access protocols using security systems, authorization levels, and real-time tracking mechanisms

I’ll emphasize that these controls aren’t just protective measures—they’re strategic tools that enhance your competitive advantage through improved accuracy and reduced losses.